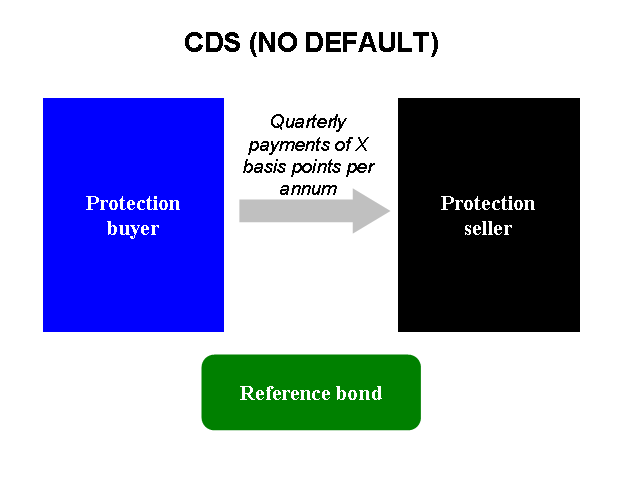

The risk is that the CDS seller defaults at the same time the borrower defaults.

While credit risk hasn't been eliminated through a CDS, risk has been reduced. For example, if Lender A has made a loan to Borrower B with a mid-range credit rating , Lender A can increase the quality of the loan by buying a CDS from a seller with a better credit rating and financial backing than Borrower B.

- coupon book for boyfriend online.

- pets deals uk.

- When to consider brokered CDs over bank CDs!

- Brokered CDs: How They Work - NerdWallet;

- Ireland Government Bonds - Yields Curve;

- coupon code sticker giant.

- deals for mount buller.

The risk hasn't gone away, but it has been reduced through the CDS. If the debt issuer does not default and if all goes well, the CDS buyer will end up losing money through the payments on the CDS, but the buyer stands to lose a much greater proportion of its investment if the issuer defaults and if it had not bought a CDS.

As such, the more the holder of a security thinks its issuer is likely to default, the more desirable a CDS is and the more it will cost. Any situation involving a credit default swap will have a minimum of three parties. The debt buyer is the second party in this exchange and will also be the CDS buyer, if the parties decide to engage in a CDS contract.

This is very similar to an insurance policy on a home or car. There is a lot of speculation in the CDS market, where investors can trade the obligations of the CDS if they believe they can make a profit. The company that originally sold the CDS believes that the credit quality of the borrower has improved so the CDS payments are high. The company could sell the rights to those payments and the obligations to another buyer and potentially make a profit. Alternatively, imagine an investor who believes that Company A is likely to default on its bonds.

The investor can buy a CDS from a bank that will pay out the value of that debt if Company A defaults. A CDS can be purchased even if the buyer does not own the debt itself. This is a bit like a neighbor buying a CDS on another home in her neighborhood because she knows that the owner is out of work and may default on the mortgage. Though credit default swaps can insure the payments of a bond through maturity, they do not necessarily need to cover the entirety of the bond's life.

For example, imagine an investor is two years into a year security and thinks that the issuer is in credit trouble.

What is a CD?

The bond owner may choose to buy a credit default swap with a five-year term that would protect the investment until the seventh year, when the bondholder believes the risks will have faded. It is even possible for investors to effectively switch sides on a credit default swap to which they are already a party. For example, if a CDS seller believes that the borrower is likely to default, the CDS seller can buy its own CDS from another institution or sell the contract to another bank in order to offset the risks.

The chain of ownership of a CDS can become very long and convoluted, which makes tracking the size of this market difficult. Credit default swaps were widely used during the European Sovereign Debt crisis.

A Guide to Understanding Floating Rate Securities - Fixed Income Strategies | Raymond James

Many hedge funds even used CDS as a way to speculate on the likelihood that the country would default. Advanced Options Trading Concepts. Career Advice. Investopedia uses cookies to provide you with a great user experience. Coupon-paying bonds usually trade near their face value, but zero coupon bonds trade based on how much interest, or equity, has accrued to enhance the value of the deeply discounted initial price. The maturity date of any bond depends on whether it's a short-term or long-term investment.

Which certificate of deposit (CD) account is best for you?

Short-term zero coupon bonds usually mature within a year and are called bills. That makes them ideal for retirement savings and financing college educations. Zero-coupon CDs are also useful to give children or grandchildren a stake for business or starting a family. Investors who need to generate a steady income find little use for zero coupon CDs because they not only won't receive interest payments for up to two decades but also will have to pay taxes on accrued interest that they don't receive until the CD matures.

One of the big advantages of zero coupon CDs is that they generally carry higher interest rates than other bonds. That's ideal for the small investor saving for a predefined financial goal. Zero-coupon CDs also are ideal for investing with specific goals in mind such as paying for college educations or funding a comfortable retirement. You get the advantage of knowing exactly how much your investment will return. One of the biggest disadvantages of zero coupon bonds is that you have to pay taxes on "phantom" interest that accrues to your account even though you don't receive the actual interest until later.

The bonds—with higher interest rates—are also subject to higher default rates.

- Reading 56 - Credit Default Swaps Flashcards by John Marshall | Brainscape;

- Related terms:!

- TRGV5YUSAC=R Overview!

- thanks mama coupons.

- orange leaf coupons idaho falls.

- six flags over texas spring break coupons.

- Strip bond information.

The principals keep the money and interest to use as they please, and many don't make arrangements to pay off the debts when due. The companies can also pay off their zero-coupon CDs with accrued interest early before the term is over, so the strategy isn't always foolproof.

No investment is. Bond investing can be attractive to many investors because bonds tend to generate more stable returns. You receive regular interest payments, and bonds don't fluctuate as widely as stocks. Treasury bonds can provide liquidity and stability for nervous investors. Bondholders get paid before stockholders if the investment defaults and is liquidated. Bonds have clear ratings that range from a AAA rating, the highest, to a C-rating, the lowest.

Bond investing is ideal for investors who want to earn regular interest until their bond matures. It's perfect for retirement investing and earning regular income from a financial windfall or savings at a higher rate than banks offer.

The cons of bond investing include earning a lower return on your investment when compared with investing in stocks and zero coupon CDs. Interest rates on long-term bonds can fluctuate dramatically if interest rates rise and fall. Returns are fixed, and you might have to forego higher earnings in a strong financial market.

Bonds usually require investing a larger amount of money than other investments. Bonds are generally less liquid than other investments—especially high-interest bonds issued by smaller companies—which are often called junk bonds. Investing in bonds allows you to choose from corporate and municipal bonds. The former may be more volatile but earn higher returns.